Planning Ahead: Why Long-Term Care Insurance Is Essential for Your Future

Long-term care insurance (LTCi) is essential for those born after 1965, as 40% of individuals needing care are under 65. Rising costs and smaller family units make planning ahead crucial. LTCi covers in-home care, assisted living, and more, while offering options like inflation protection and return-of-premium riders. These features ensure financial security, protect loved ones, and provide tax advantages. Learn how proactive planning with LTCi safeguards your future and brings peace of mind. Contact TouchPoint Solutions to explore your options today!

The Growing Need for Long-Term Care Insurance: A Case Study

Long-term care insurance (LTCi) is rapidly becoming a financial necessity for individuals born after 1965. While often associated with seniors, the need for long-term care (LTC) services is increasingly prevalent among younger Americans. Without adequate coverage, many face significant financial and emotional strain. This blog explores how LTCi works, its benefits, and why investing in it early is a smart choice.

The Problem: Rising Demand for Long-Term Care Among Younger Americans

Contrary to popular belief, long-term care isn’t just for the elderly. In fact, 40% of individuals currently needing LTC services are under the age of 65. Younger Americans facing accidents, chronic illnesses, or disabilities often require assistance with activities of daily living (ADLs), such as bathing, dressing, and mobility.

Key statistics highlight the urgency of planning ahead:

70% of individuals turning 65 will need long-term care at some point, but the demand for younger people is steadily growing.

The average cost of home health care is $54,912 annually, and nursing home costs often exceed $100,000 per year.

Without insurance, these expenses can quickly deplete savings and disrupt retirement planning.

The Solution: Planning for Long-Term Care Early

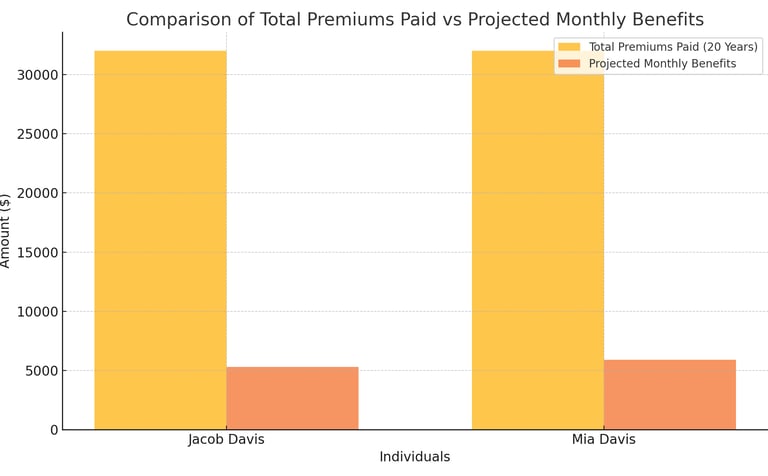

Case Study: Jacob and Mia Davis

Meet Jacob, aged 42, and Mia, aged 45, realized the potential financial risks of needing long-term care and decided to invest in LTCi. Here’s a breakdown of their policy and benefits:

Jacob Davis:

Annual Premium: $1,600

Total Premium Paid Over 20 Years: $32,000

Projected Monthly Benefit by Age 62: $5,300

Unused Benefits: With a return-of-premium rider, unused funds can be transferred tax-free to beneficiaries or to Mia.

Mia Davis:

Annual Premium: $1,600

Total Premium Paid Over 20 Years: $32,000

Projected Monthly Benefit by Age 65: $5,900

Shared Care Rider: Allows her to access Jacob’s policy if her own is exhausted.

Even if they never use their policies, the return-of-premium rider ensures their investments aren’t wasted, offering peace of mind that their loved ones will benefit from their foresight.

Why LTCi Is Essential for Generation X and Beyond

Investing in LTCi provides a range of benefits:

Financial Security: Protects savings and retirement funds from being depleted by care costs.

Flexibility: Policies can be tailored with riders for inflation protection, shared care, and unused benefit returns.

Peace of Mind: Ensures access to quality care without burdening family members emotionally or financially.

Call to Action: Plan Your Future Today

Don’t wait until a care need arises. Contact TouchPoint Solutions for a personalized consultation to explore LTCi options. Together, we’ll help you secure your future, protect your family, and provide peace of mind for years to come.